Storm Ingunn and the two-speed salmon market: Why quality, not just supply, shaped prices.

When Storm Ingunn battered Norway’s coastline in late January 2024, industry observers braced for a textbook oversupply crisis.

While casual observers might expect that early harvesting as a result of the storm would flood the market with fish, leading to an immediate price drop, what actually unfolded was more complex, revealing a divergence in how different segments of the salmon market responded.

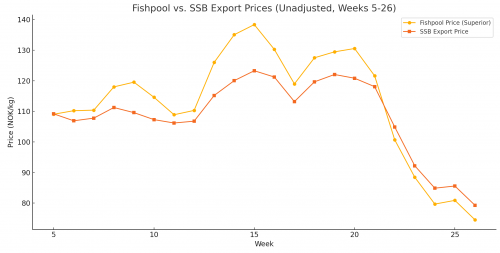

While Statistics Norway (SSB) export prices softened, the Fishpool price for superior-grade whole salmon surged to its highest ever level. Rather than a simple oversupply shock, Storm Ingunn (acting alongside an already severe winter sores crisis) fractured the salmon market into two distinct pricing tiers.

The missing piece in this puzzle? Norwegian export regulations prevent the direct export of lower-quality “production fish.” Instead, downgraded fish must first be processed—usually into fillets—before entering export markets. This means that SSB prices reflect both whole salmon and processed fish, while Fishpool prices track only superior-grade whole salmon.

All figures in this analysis reflect raw, unadjusted prices from 2024, ensuring that the observed trends are based purely on market movements without inflation adjustments.

A Growing Price Divide: Whole vs. Processed Fish

In the immediate aftermath of the storm, SSB export prices and Fishpool prices were relatively aligned, but by early spring, the market began to split. The price gap widened, reflecting a growing scarcity of premium whole fish as more downgraded fish entered processing.

- Week 9 (one month after the storm):

- Fishpool price: 119.54 NOK/kg

- SSB export price: 109.58 NOK/kg (A gap of 9.96 NOK/kg—early signs of market divergence)

- Week 13:

- Fishpool price: 126.01 NOK/kg

- SSB export price: 115.19 NOK/kg

- Week 14:

- Fishpool price: 135.06 NOK/kg

- SSB export price: 120.04 NOK/kg (A 15.02 NOK/kg gap—peak disparity, premium salmon tightening)

- Week 15 (highest recorded price gap):

- Fishpool price: 138.37 NOK/kg

- SSB export price: 123.28 NOK/kg (A record 15.09 NOK/kg gap—highlighting market segmentation)

This progression suggests that while initial supply disruptions were limited, the ongoing scarcity of superior whole salmon intensified over time, reaching its peak by mid-April. Meanwhile, the SSB price remained lower, reflecting an increase in the share of processed, downgraded fish in the broader export mix.

Why Was Superior Salmon Scarce After the Storm?

Storm Ingunn’s effect on fish wasn’t just about quantity—it was about damage.

- Hurricane-force winds (115 mph) battered salmon pens, increasing stress and mechanical injuries.

- Fish suffering from bruising or deformities were downgraded to “production” fish.

- Norwegian regulations prohibit the direct export of downgraded fish, meaning they had to be processed before being sold abroad.

Instead of an oversupply of whole salmon, the storm disrupted the availability of superior-grade fish, creating a split market where premium fish remained expensive while processed fish weighed down the overall export price.

Where Did the Rest of the Fish Go?

One of the biggest surprises in the data is that fresh salmon exports didn’t surge in the immediate aftermath of the storm.

- Week 5 fresh exports: 13,511 tonnes (down 20% from 2019’s level of 16,333 tonnes)

- Week 6 fresh exports rose to 15,862 tonnes, but

- By Week 8, they had fallen to just 10,687 tonnes—the lowest February figure in years.

Meanwhile, frozen salmon exports steadily increased:

- Week 5 frozen exports: 342 tonnes

- Week 6: 487 tonnes (42% increase in a single week)

- By Week 9: 441 tonnes, nearly double the early-February level.

The takeaway? Instead of an immediate flood of fresh salmon hitting export markets, more fish were processed or stored.

A Two-Speed Market: Premium vs. Processed

By late February, Norway’s salmon market had split into two pricing tiers:

- Superior whole salmon (Fishpool price) became increasingly scarce, forcing buyers to pay more.

- Lower-quality fish dominated the broader export mix, pulling down SSB prices, which included processed production fish.

Rather than a classic oversupply event, Storm Ingunn distorted the quality mix of available fish, leading to a rising premium for superior-grade salmon while processed fish pushed down export prices.

The Delayed Reckoning: How the Storm May Have Contributed to the June Price Collapse

By early summer, the effects of Storm Ingunn’s quality distortions had begun to unwind. While the immediate glut of production fish was partially absorbed through processing, this didn’t mean the market had fully stabilized. Instead, the delayed impact of early harvesting, inventory build-ups, and weaker demand conditions created the conditions for a record-breaking price crash in June.

Several factors likely connected the February distortions to the June collapse:

- An artificial tightening of superior-grade supply in Q1 led to inflated Fishpool prices.

- With fewer whole premium fish available post-storm, buyers had to pay a premium.

- This created a false sense of market strength—prices remained high even as more fish entered processing.

- Processors accumulated frozen and processed inventories, creating a delayed market impact.

- Rather than flooding the market in February, much of the downgraded fish was stored or processed, preventing an immediate price collapse.

- By June, those stocks were finally released into the market, compounding the seasonal harvest surge.

- When demand softened, processors and traders had little room to maneuver.

- Key buyers—particularly in Europe and Asia—had already stocked up heavily in early 2024, betting on price stability.

- When fresh supply surged in June, inventories were already full, and prices collapsed under the weight of excess supply.

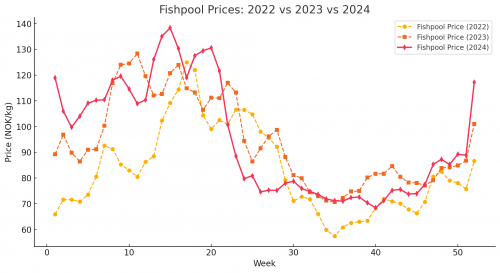

The result? A record-breaking 56.01 NOK/kg drop (from Week 20: 130.55 NOK/kg to Week 26: 74.54 NOK/kg) in fresh whole salmon prices—the largest monthly price decline ever recorded.

The Storm’s True Legacy

Storm Ingunn was not just an oversupply event—it was a market segmentation event. While total salmon availability remained high, the storm selectively removed superior-grade fish from the market, creating a premium-tier shortage (exacerbated by the earlier winter sores crisis) that pushed Fishpool prices to record levels.

However, by delaying the release of production fish into the market through processing and storage, the true oversupply issue was postponed rather than avoided. When these stocks re-entered the market alongside the seasonal summer harvest, the price collapse was sharper than any single event could have caused alone.

Because in a market where price is shaped as much by quality as by quantity, the real lesson of Storm Ingunn is that a storm doesn’t just increase supply—it reshapes it, sometimes with consequences that only become clear months later.